Conventional vs Non-Conventional Mortgages explained by a Multi-Media Digital Mortgage Broker in Catonsville. Although I have 28 years experience I still have a difficult time explaining the different types and classifications of mortgages because the differemnt classifications or categories sound similar. So in order to bring better clarity and shed light on the subject I created a InfoGraphic that is included below.

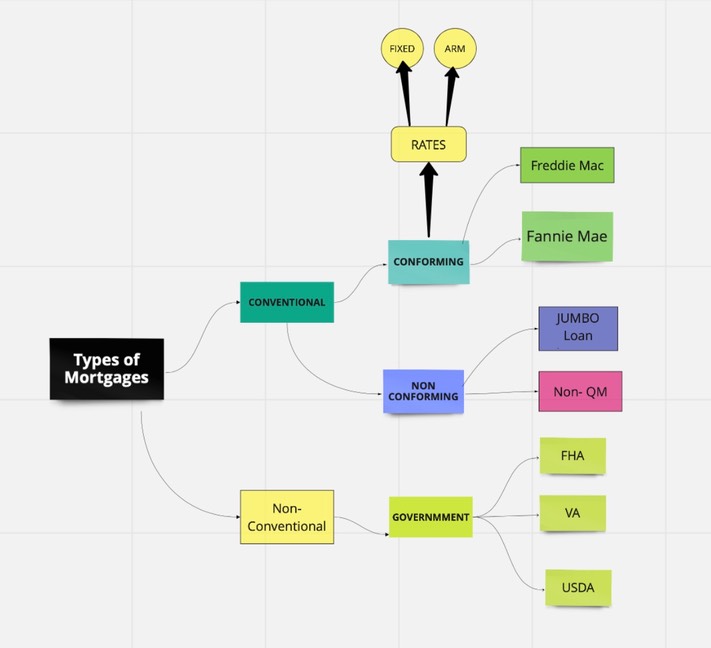

There are two major classifications of Mortgage Loans: Conventional & Non-Conventional.

A Conventional loan is a mortgage loan that's NOT backed by a government agency. There are two categories of Conventional mortgages: “Conforming” and “Non-Conforming” loans.

All Conforming Loans are sold to Fannie Mae (Federal National Mortgage Association -FNMA) or Freddie Mac (Federal Home Loan Mortgage Corporation FHLMC) and conform to their rules.

All other Loans are Nonconforming.

ALL “Nonconforming” loans fall outside of the “Conforming: loan rules.

All Government backed loans. FHA, VA, USDA, are Non-Conventional and also Non-Conforming

Loan Amounts above conforming limits: JUMBO loans include higher loan amounts

A Non-QM or a non-qualified mortgage is a home loan that is not required to meet agency-standard documentation requirements as outlined by the Consumer Financial Protection Bureau (CFPB). Non-QM Mortgages are Non Conforming and can have Slackened Credit Requirements:

THE CONFORMING LOAN EXPLANED

A Lender is like a grocery store. In the grocery store model, the merchant will buy product from producers and sell out to the public at retail. When he receives the proceeds of the sale, the excess realized over his cost is his profit. With the cost portion of the sale he has the ability to buy more product. This frees up his funds so he can get more product and service more buyers: then, rinse and repeat.

The Lender - Merchant is organized a bit different. In this money supermarket, the items for sale are Mortgage Loans. The merchant or the lender has a finite amount of cash on hand to make mortgages. So when a mortgage is created, he gets a written assurance of a pay-back with interest. This written assurance is called a note. You cannot buy replacement inventory for mortgages with a written promise. So a mechanism was created to sell these notes to investors.Two United States government-sponsored enterprises (GSE) were created. Federal Home Loan Mortgage Corporation (FHLMC), commonly known as Freddie Mac, and Federal National Mortgage Association -FNMA commonly known as Fannie Mae. Both are publicly traded, government-sponsored enterprises (GSE), Both are publicly held companies. These are referred to as Quasi-Public Corporations. A quasi-public corporation is a company in the private sector that is supported by the government with a public mandate to provide a given service. A quasi-public corporation’s priority is its government mandate rather than value and profit for shareholders.This contrasts to the normal corporate mandate of answering to the shareholders first. Fannie Mae and Freddie Mac set the guidelines that Conforming loans must follow. The best-known rules are: 20% Down Payment, the maximum size of the loan and stricter credit requirements. Since the agencies will only guarantee 80% in case of a default, a third party will guarantee the shortfall thru a Private Mortgage Insurance Policy. You can put less than 20% Down but you will need to get Private Mortgage Insurance (PMI). However, over the years many programs have been instituted to create preferential treatment to government designated victim groups.The quest is for the “greater good” but many times this government mandate leads to malinvestment. However, if you fall into this bucket, pursue your dream while the opportunity is still available.

Private Mortgage Insurance

The Agencies ( Fannie mAe & Freddie Mac) guarantees the lender up to an 80% of the initial loan amount. PMI protects your mortgage lendersfor the balance of the loan in case in case of a default. The cost for PMI varies based on the borrower’s credit score, loan type and the size of the down payment.

PMI does not last forever. When you reach 20% equity in the home from your amortization schedule, you can petition your lender to remove the PMI from your mortgage payments.

If your home has increased in value such that the equity reaches 20, you should contact your lender to have them recalculate your PMI requirement. They may insist on a new appraisal so they can use the verified value.

However, when the equity in the home reaches 22%, your lender will automatically remove PMI from your loan.

ADRIAN CITRONI - MORTGAGE BROKER

Primary Service Area: Catonsville & Vicinity

Academy Heights, Arbutus - Halethorpe, Catonsville, College Hills, Elkridge, Ellicott City, Oella, Westchester

Licensed Loan Originator NMLS# 144522; MD - DC - PA - DE - VA - FL - CA

CALL OR TEXT: 410-916-0776